FG Trade/GettyImages; Illustration by Hunter Newton/Bankrate

Key takeaways

- One way to clear medical debt is to tap into your home’s equity via a HELOC.

- HELOCs offer flexible repayment periods with few restrictions and lower interest rates than personal loans or credit cards.

- On the downside, HELOCs put your home at risk if you can’t make payments, and their variable interest rates can make payments jump in size.

Medical bills are a mounting disease in this country. According to data from the Kaiser Family Foundation (KFF), an estimated 14 million people, or 6 percent of U.S. adults, owe over $1,000 in medical debt. Roughly 3 million Americans have more than $10,000 in medical debt.

On the other side of the equation, many Americans are sitting on a substantial source of funds: their home. Thanks to rising property values, the average U.S. homeowner now has more than $298,000 in home equity, according to CoreLogic.

For those burdened by medical bills, borrowing against that equity could offer some relief, and one easy way to do it is via a home equity line of credit (HELOC). But while it’s tempting to tap that ownership stake, is it advisable to use your home equity to pay medical expenses? Let’s do a check-up.

How using a HELOC to pay medical bills works

A HELOC is a revolving form of credit. Functioning much like a giant credit card, it gives homeowners flexibility around both borrowing and repaying funds.

Most lenders require at least 15 percent to 20 percent equity in your home to obtain a HELOC, and your credit limit depends on several factors, including your credit and outstanding debts, the value of your home and the amount you owe on your mortgage. Once approved, you’ll be given a line of credit up to 85 percent of the appraised value of your home, minus your outstanding mortgage balance.

Once the line of credit is established, you can withdraw sums on a rolling basis, making repayments monthly. Depending on your lender, there might be a minimum or maximum withdrawal requirement after your account is opened. Your lender might offer access to those funds in a variety of ways, including through an online transfer, writing a check or using a credit card connected to your account.

Even with bad credit, you can get a HELOC to pay your health-care bills. Of course, the stronger your credit score and financials, the better the interest rate and terms will be.

Pros and cons of using a HELOC for medical bills

A HELOC might sound like the solution to wiping out medical expenses, but as with any financial strategy, there are advantages and drawbacks.

EXPAND

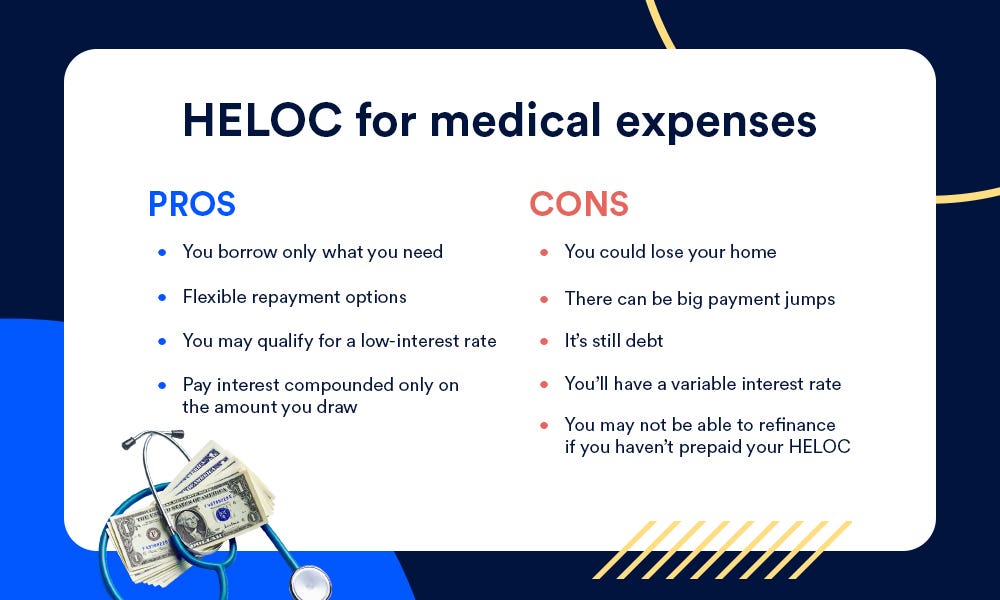

Pros

- You borrow only what you need. During the draw period, you can withdraw as much funds as necessary (within your limit) to pay for medical expenses as they come up. This system contrasts with a home equity loan, which gives you a fixed lump sum.

- Pay interest only on the sums you draw. With many HELOCs, you have the option to pay back just the interest (rather than interest and principal) during the draw period. Also, you’ll only pay interest on the amount you actually use — again, in contrast to a home equity loan, whose repayments start immediately.

- Comparatively low-cost loan. While your exact APR will depend on the lender and your creditworthiness, HELOCs typically have much lower interest rates than credit cards or personal loans.

- Long repayment options. The timeline for your HELOC can vary depending on the amount you borrow and your lender, but typically lasts 20 or 30 years. Repaid principal goes to refresh the credit line, and you can borrow that money again.

Cons

- You could lose your home. The biggest drawback of a HELOC: It’s a secured loan, backed by your home, meaning you could lose it to foreclosure if you don’t make timely payments. Another serious thorn: If home values fall, you could owe more on your home than it’s worth (in other words, have negative equity).

- You’ll have a variable interest rate. HELOCs usually come with fluctuating interest rates, meaning they can change up or down over time. That means your monthly payments can vary and, if interest rates rise in general, you’ll be paying increasing amounts, pinching your budget.

- There can be big payment jumps. Rising interest rates aren’t the only problem. Your minimum monthly payments are going to make a big leap — often doubling at least — once you enter the repayment period, as they’ll include both principal and interest. Also, your HELOC might come with a balloon payment when the draw period ends — a large lump-sum payment of the outstanding balance. Generally, a balloon payment can be tens of thousands of dollars.

- You might not be able to refinance. If you’re thinking about using home equity for unexpected medical expenses, know that you might have to get approval from your HELOC lender to refinance your mortgage loan — and they could refuse until you pay off the line of credit. Should you sell your home, you’d probably have to settle the HELOC immediately too, cutting into your proceeds.

- It’s still debt. Using a HELOC for medical expenses essentially replaces unsecured debt with secured debt: It’s shifting your burden, but not eliminating it. You might find you’re making mortgage and HELOC payments — not to mention other regular bills — all at the same time, and the increased debt load could hurt your credit score. (Of course, having unpaid medical bills sent to collections isn’t going to do your credit profile any good, either.)

What to consider before using your home’s equity to pay for medical bills

Using home equity for medical expenses shouldn’t be your first option. While it can give you access to cash fast, there are a number of downsides and risks. If you’re thinking about using your home’s equity to cover your medical debt, here are a few alternatives you might consider.

Payment plans

Many hospitals and medical providers will work with patients to establish a payment plan. A payment plan will help you pay off your medical debt overtime in smaller installments that are more manageable than a lump sum. The monthly payment and repayment term can usually be negotiated with the provider. Make sure to ask about any interest charges or fees required when setting up a payment plan.

Assistance programs

Medical assistance programs can be a great resource for many people with medical debt. Some organizations, like the The Healthwell Foundation and Patient Access Network (PAN) Foundation, provide grants that can help you pay off your debt more quickly. These groups can also connect you with resources to negotiate your medical debt or help you get more affordable health care. (See “Tips for paying off medical bills,” below.)

Bill negotiations

Getting a bill reduction might be as simple as calling your doctor’s billing department. Ultimately, doctors and hospitals want to get paid for their services, so they might be willing to relieve some of your debt if you’re unable to pay it off entirely. If you need help negotiating your medical bills, consider working with an advocacy group or non-profit that specializes in debt relief. However, some of these organizations might charge a fee for their services.

Common medical costs

A 2023 Urban Institute study found that most of Americans’ past-due medical debt relates to hospital care. Just three days in the hospital can cost you an average of $30,000, according to Healthcare.gov. Check out these common procedures and the typical cost associated with each — many in the tens of thousands of dollars:

| Procedure | Average cost (without insurance) |

|---|---|

| Source: Debt.org | |

| Heart bypass surgery | $123,000 |

| Hip replacement | $40,364 |

| Angioplasty | $28,2000 |

| Gastric bypass | $25,000 |

| Cataract surgery | $3,500 – $7,000 |

| Tonsillectomy | $4,000 – $6,000 |

| Appendectomy | $33,000 – $48,000 |

| Emergency fracture surgery | $15,000 – $35,000 |

Tips for paying off medical bills

It’s important to know your rights when it comes to medical bills. According to the Consumer Finance Protection Bureau, if you’re paying for care out-of-pocket, your provider must give you a good-faith estimate of how much the services will cost. If your bill is $400 or higher than the estimate you received before services, you might be eligible to dispute it.

Even with health insurance, it’s always good to ask for a cost breakdown in advance, anyway, and an itemized list of services and treatments afterwards.

Keep in mind: The No Surprises Act of 2022 protects patients with health insurance coverage. It bans unexpected bills from out-of-network providers or facilities — that is, if you were not informed the place was not part of your plan’s network, and/or didn’t consent to or authorize its services.

Aside from obtaining a HELOC, here are a few other ways to avoid or minimize the medical debt:

- Comparison shop. Even if you have health insurance, you can still shop for a healthcare provider. If you have a preferred provider option (PPO) health insurance plan, you’ll pay less visiting a doctor or hospital that’s part of your insurer’s preferred network of providers.

- Review your health coverage. Go over your health insurance policy to see what’s covered and what isn’t. All covered expenses should be paid for by your provider. Keep an eye out for balanced billing: That’s when a hospital or provider tries to charge you the difference between their standard rates and the rates they’ve negotiated with your health insurance company.

- Review your medical bills. “It’s estimated that about 60 percent of medical bills that are issued have errors,” says Braden Pan, CEO of Resolve Medical Bills, a patient advocacy firm. “There are two types of billing errors: charges for services not provided and hidden charges. To identify charges for services not provided, review your itemized bill and consult your electronic medical record (EMR) if needed. To detect hidden charges, use tools like Find-A-Code to check for incorrect code pairs. Research the CPT codes and consult resources such as the American College of Emergency Physicians” and the Healthcare Bluebook, an online comparison tool for medical services.

- Establish a payment plan. In addition, many medical offices offer payment plans. More often than not, health care staff want to work with you to make repayment manageable and in installments — often with no interest.

- Seek out additional help. Depending on your income, you may qualify for special relief. “If you’re dealing with children’s medical bills, the State Children’s Health Insurance Program (CHIP) may offer assistance,” Pan says. “When it comes to expensive drugs, pharmaceutical companies often have assistance programs for individuals with financial need. It’s worth reaching out to the drug manufacturer and inquiring about grant programs.” He also cites several private charities, “organizations like PanFoundation, Healthwell Foundation, Leukemia & Lymphoma Society and CancerCare [that] offer aid for various medical conditions.”

- Establish a health savings account (HSA). If your insurance plan allows, take advantage of an HSA to save tax-free money to pay out-of-pocket medical expenses.

- Claim tax deductions for medical expenses. If your unreimbursed, out-of-pocket medical bills exceed 7.5 percent of your adjusted gross income, you might be able to deduct them from your taxes (you’ll have to itemize deductions on your return).

Additional reporting by Elizabeth Rivelli

link

More Stories

Without subsidies, Florida families cringe over health insurance bills

Medicare Advantage Insurers Face New Curbs on Overcharges in Trump Plan That Reins in Payments

Doctors question 6-minute X-ray rule for health insurance payment